Subsidies Series: Part II

Photo by Mathias Reding on Unsplash

As climate change dominates the news, reports of ‘generous’ subsidies to fossil fuel and renewable energy industries have become commonplace. But journalistic publications and media companies have done a poor job reporting subsidies accurately, leading many leaders and politicians to make incorrect conclusions and those misinformed conclusions are then amplified by social media.

The inundation of half-truths and outright lies has been perpetrated at scale. This has resulted in dangerous groupthink. The widely held untruths of what a subsidy is, what governmental subsidy programs do, and the level of total subsidies per unit of usable energy has harmed the national consciousness surrounding energy policy.

This subsidies series will present research in an attempt to illuminate the many untruths, define what a subsidy is and what a subsidy is not, explain the various subsidy programs supporting each primary fuel, and demonstrate each subsidy’s impact. Let me be clear, though; subsidies are not inherently good or bad. Thus, our research does not make any moral argument for or against any particular subsidy other than whether it is achieving its purpose.

Subsidies Series Part II - EIA Data

In Part I, we explored how definitions matter. As we begin examining the EIA’s data this week, remember that the EIA’s definition of what a subsidy is expanded upon the Merriam-Webster definition when it chooses to include Tax Breaks.

If you Google “fossil fuel subsidies“ you’ll find 34.5 million results and 29.1 million results for “oil and gas subsidies.” If you Google “renewable energy subsidies” you’ll find only 12.7 million results and only 6.85 million for “wind and solar subsidies.”

If Google is any indication, society incorrectly assumes that fossil fuels receive more subsidies than renewable energies. This week we will examine the truth about subsidies via the EIA’s most recent Financial Interventions and Subsidies report (updated 2018).

EIA Financial Interventions and Subsidies

These four EIA categories can actually be re-categorized into two: (1) Tax Breaks and (2) Direct Subsidies. Tax Expenditures being the former, and the rest are able to be categorized as the latter. You will quickly notice that the vast majority of dollars are allocated to Tax Expenditures, where wind and solar dominate the space, and Direct Expenditures, where Biofuels dominated in 2013 before giving way to wind and solar in the fiscal years 2013 and 2016.

Visualized in a different way below, you can see each fuel’s respective total subsidies over the three most recent reporting years.

Our research also shows that in the fiscal year 2016, natural gas and petroleum liquids actually lost money on Tax Breaks (graphic below).

You might wonder if this is a typo or flaw in the data. It is not. As the EIA writes in its most recent subsidies and financial interventions report:

“NATURAL GAS AND PETROLEUM-RELATED U.S. TAX EXPENDITURES DECREASED FROM $2.3 BILLION IN FY 2013 TO AN ESTIMATED REVENUE INFLOW (VERSUS A POSITIVE TAX EXPENDITURE) OF $940 MILLION IN FY 2016, THUS IN AGGREGATE BECOMING A SET OF REVENUE-GENERATING TAX PROVISIONS TO THE GOVERNMENT IN THAT FISCAL YEAR.”

You have probably never heard this before, and neither had we before doing this research. We will now review each of the four categories reported by the EIA in order of least funding to the most funding.

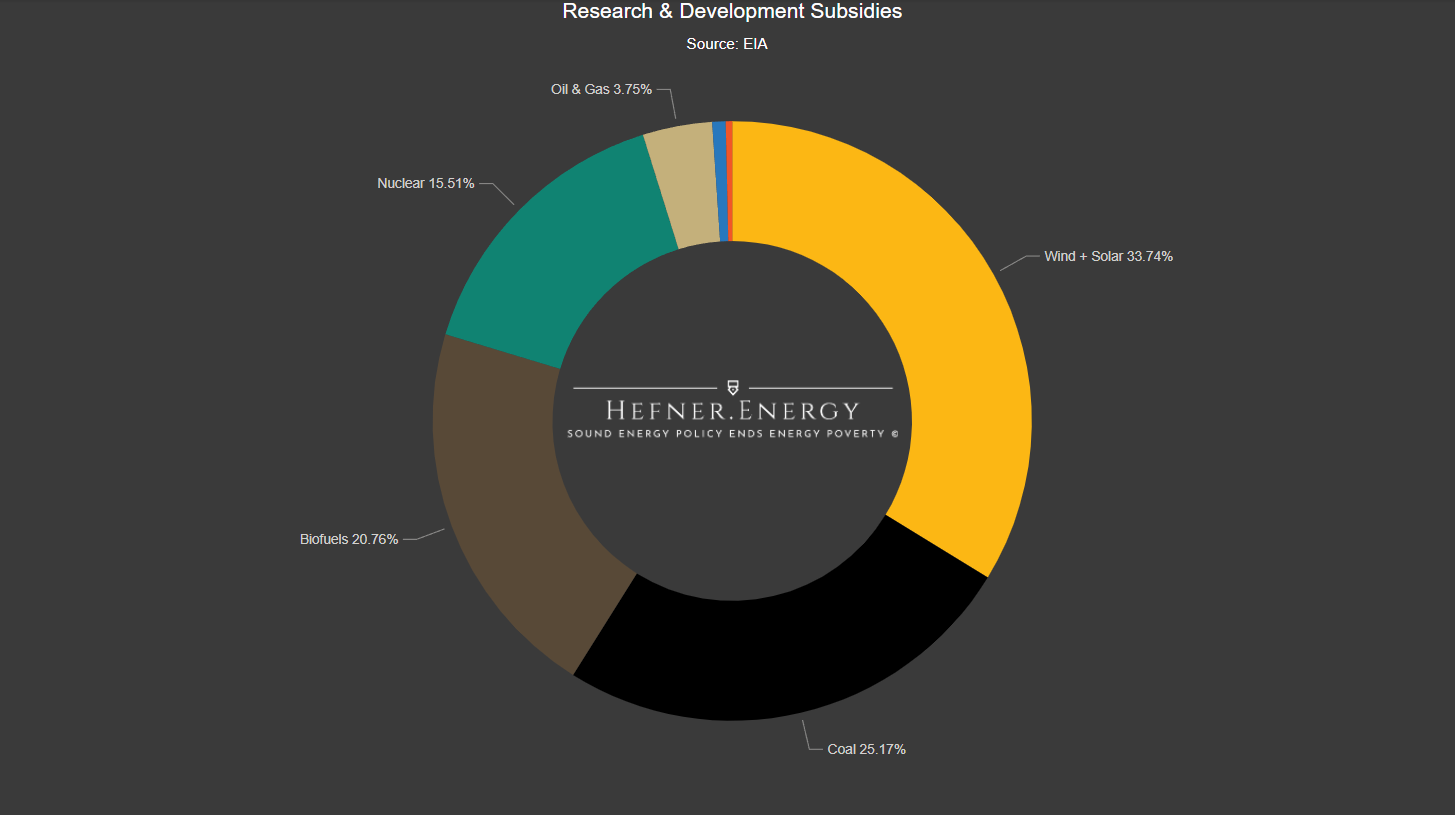

Research & Development, a Direct Subsidy

Research and development totals approximately $1 billion per year and is somewhat evenly distributed across the fuel categories. Wind, solar, and nuclear benefit the most for all years reported. However, the even distribution breaks down in the most recent year reported.

In the fiscal year 2016, coal benefitted the most from government research and development. The $337 million allocated in FY 2016 is for clean coal power initiatives. Oil and gas is a small sliver of total funding at 6.09% (or $56 million), while wind and solar receive 25.35% (or $233 million).

By contrast, oil and natural gas at just 3.75% is not showing to have received much government support from research and development funding.

DOE Loan Guarantees, a Direct Subsidy

No DOE Loan Guarantees were awarded in the most recent year of EIA data. In the fiscal years 2010 and 2013, DOE Loan Guarantees were nearly all dedicated to wind, solar, and nuclear. No DOE loan guarantees benefitted a fossil fuel.

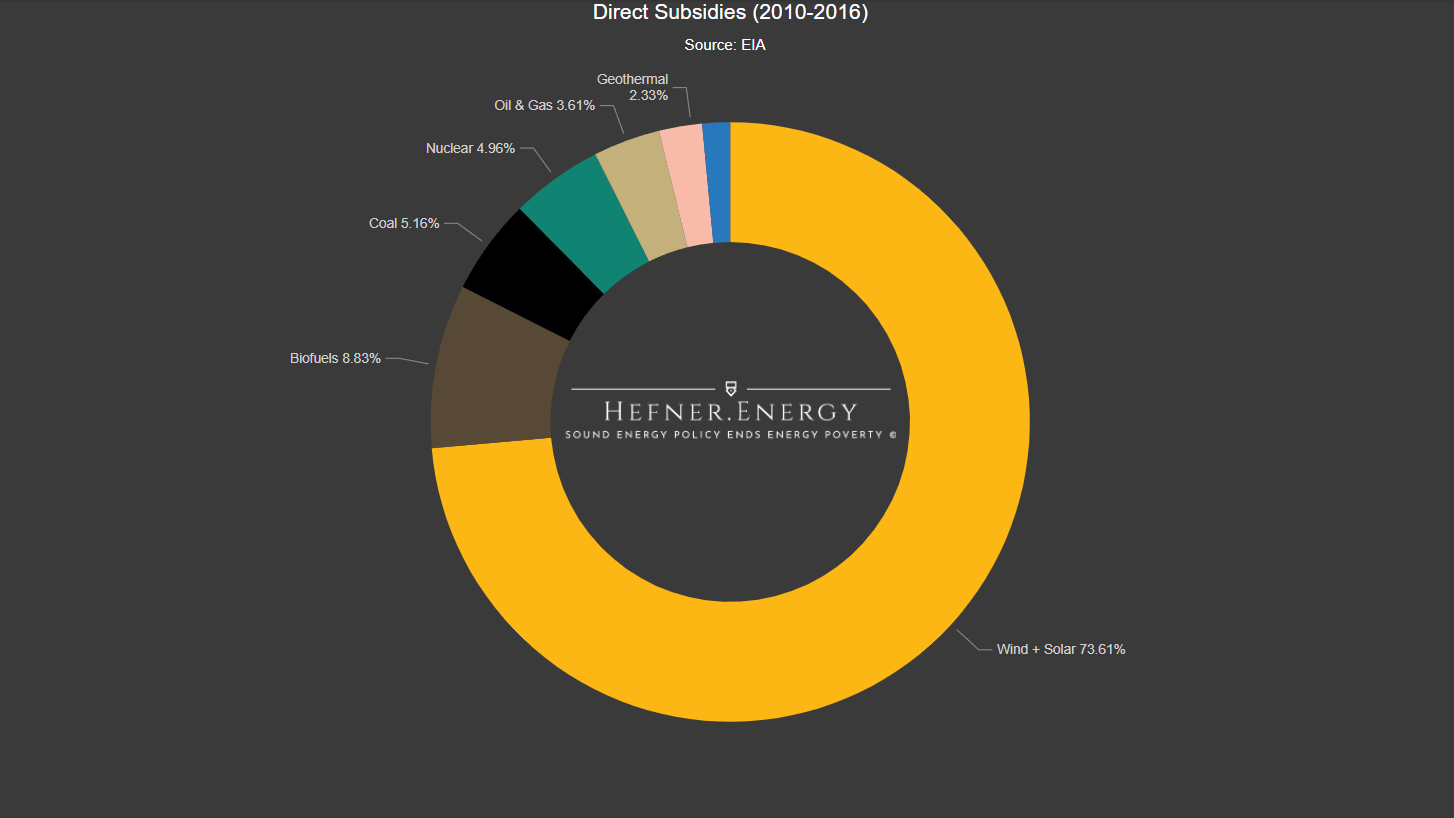

Direct Expenditures, a Direct Subsidy

Direct expenditures are in the form of cash, too, just like R&D and DOE Loan Guarantees by the federal government.

The pie chart for Direct Expenditures reveals that wind and solar receive the lion’s share, taking an astonishing 83.4% of cash handed out by the federal government. Biofuels received 6.52% of the subsidies, and oil and natural gas at just 3.72%.

However, when we examine the direct expenditure programs earmarked for oil and gas, we find that they do not benefit oil and gas companies at all.

Direct Expenditures Programs for Oil & Gas

U.S. Department of Agriculture - $6 million

The total is to the benefit of the Denali Commission Program, which benefits Alaskans and connects rural communities.

U.S. Department of Energy - $3 million

This funding goes to the benefit of the Industrial Carbon Capture and Storage (CCS) Application.

U.S. Department of the Interior - $17 million

This goes to the federal government to manage its oil and gas interests and for tribal coordination.

U.S. Department of Transportation - $42 million

These funds go to pipeline safety for the United States.

U.S. Environmental Protection Agency - $44 million

These funds go to the National Clean Diesel Emissions Reduction Program and State Clean Diesel Grant Program.

Thus, oil and gas companies do not receive a single dollar of Direct Subsidies from the U.S. federal government. The EIA confirmed this to me via email,

“WE ARE NOT AWARE THAT THERE ARE ANY DIRECT FEDERAL SUBSIDIES FOR GENERATING ELECTRICITY WITH PETROLEUM LIQUIDS (OR NATURAL GAS).”

- Office of Stakeholder Outreach and Communications, U.S. EIA representative to Hefner.Energy via email on March 16, 2022

That’s why one prominent oil and gas chief executive is accurate when he says, “now my recollection of what a subsidy means is when you are given money to do something. I guess when I drilled 17 dry holes in a row I missed that pay window. No one sent me a check.” What’s often missed in this executive’s comment is that he risked his own dollars and those of his investors to drill those oil and gas wells. He did not risk taxpayer dollars.

Direct Expenditures for Wind + Solar

The wind and solar industries have taken significant direct subsidies from taxpayers – totaling $13 billion in the most recent three years reported by the EIA.

Table 16 of the EIA Financial Interventions and Subsidies report outlines these programs:

The vast majority, 90%, of dollars attributed to renewable energies are in the form of bonds given to wind and solar companies, totaling $4.678 billion out of the $5.732 billion in FY 2010, $8.514 billion of the $8.716 billion in FY 2013 (being 98%), and $820 million out of the total $909 million in FY 2016. Unlike Direct Expenditures for oil and gas, these dollars do flow directly to solar and wind companies.

Tax Breaks (Tax Expenditures)

So far all of the previous analysis was focused on the Merriam-Webster definition of a “subsidy”. This is the section of the analysis that expands the dictionary’s definition to include Tax Breaks as a subsidy.

Direct Subsidies as researched herein account for $19.698 billion from the federal government from 2010-2016:

$14.499 billion of which was allocated to Wind + Solar,

$1.74 billion of which was allocated to Biofuels,

$1.071 billion of which was allocated to Coal,

$977 million of which was allocated to Nuclear,

$712 million of which was misattributed to Oil + Gas,

$458 million of which was allocated to Geothermal, and

$295 million of which was allocated to Hydroelectric

By comparison, Tax Breaks alone account for $28.695 billion, 146% more than that of all the Direct Subsidies combined.

Biofuel Tax Breaks: $12 Billion

Biofuels receive the lion’s share of federal tax breaks at $12 billion.

The largest tax provision benefitting biofuels comes from 26 USC 6426 the Biodiesel Producer Tax Credit valued at $2.65 billion in FY 2016 and $4.856 billion from 2010-2016 – by itself equaling more than the entirety of the oil and gas industry’s tax breaks over the same period of time.

Wind + Solar Tax Breaks: $7.8 billion

Wind and solar received $7.8 billion in Tax Breaks, with $2.5 billion in FY 2016, making them the second-largest benefactor of tax breaks behind Biofuels.

The largest programs benefitting wind and solar are known as the Production Tax Credit (PTC) and Investment Tax Credit (ITC) which together helped wind and solar production by $8.1 billion. The PTC, frequently referred to as Section 45, provides a tax credit of $0.024 per kilowatt-hour (kWh) of electricity generation produced. For context, the industrial price of electricity in the United States is $0.066 per kWh. The ITC, frequently referred to as Section 48, allows 26 percent of any solar installation to be written off against a company’s income.

Together these two programs are projected to cost taxpayers $107 billion between 2022 and 2031. That’s 2,229% of the total amount of tax breaks for the oil and gas industry and 5,194% of the tax breaks received by oil and gas producers from 2010 to 2016, and that is assuming non-production incentives are included.

Oil + Gas Tax Breaks: $4.288 billion

Oil and gas tax breaks totaled $4.288 billion in the three most recent years reported by the EIA, being roughly one-third that of Biofuels.

Table 8 of the EIA Financial Interventions & Subsidies report highlights all the natural gas and petroleum-related energy-specific tax expenditures. Remember, in the fiscal year 2016, the oil and gas tax breaks were a source of revenue for the federal government, totaling $940 million to taxpayers.

We will walk through each of the oil and gas specific tax breaks together (from largest to smallest, on average, over the past three years reported by the EIA).

Alternative Fuel and Fuel Mixture Credit (26 U.S. Code § 6426

The largest “fossil fuel subsidy” is largely a subsidy for transportation. Common nontaxable uses in a motor vehicle are: on a farm for farming purposes; in certain intercity and local buses; in a school bus; for exclusive use by a non-profit educational organization; and for exclusive use by a state, political subdivision of a state, or the District of Columbia.

As 26 U.S. Code 6426 reads, it is a credit for “alcohol fuel, biodiesel, and alternative fuel mixtures.” Alternative Fuels Credit is defined to include the following fuels:

Liquified petroleum gas (LPG)

Compressed Natural Gas (CNG)

Liquified natural gas (LNG)

Dual Fuel Vehicles

Liquified Hydrogen (LH)

Carbon Capture Fuels

Liquid fuels derived from biomass

None of these fuels benefit or incentivize oil production. It is debatable whether any of these fuels incentivize natural gas production.

The Fuel Mixture Credit only applies to liquified hydrogen, compressed or liquified gas derived from biomass, and liquid fuel derived from biomass. It specifically excludes any fuels that are derived from fossil fuels.

Many of these fuels have nothing to do with natural gas production. Yet all of their credits are credited by the EIA against “Natural Gas & Petroleum Tax Expenditures.”

Both of these programs expired on December 31, 2021.

Percentage Depletion (26 U.S. Code § 613)

This portion of the tax code has been a feature available to multiple industries since 1926. Percentage depletion is a concept that every industry uses in principle, known as depreciation.

As it applies to oil and gas, this provision supports independent producers (businesses with 11 or fewer employees) to produce oil and gas that would otherwise be uneconomic.

Different industries are able to depreciate associated produced reserves at a set percentage rate, with no company able to depreciate more than 100 percent of the taxpayer’s income from the property.

The various percentage depletion industries are as follows:

22% Sulphr and uranium;

15% gold, silver, copper, iron ore, and oil shale;

14% metal mines;

10% asbestos, brucite, coal, lignite, perlite, sodium chloride, and wollastonite;

7.5% clay and shale used for manufacturing sewer pipe or brick;

5% gravel, peat, pumice, sand, scoria, shale (except shale oil), and stone;

14% anything not specifically listed above.

The Percentage Depletion feature of the tax code benefits the more than 10 million mineral and royalty owners in the United States as well as the more than 15% of United States production.

To suggest this is just an “oil and gas subsidy” is misinformation. In fact, Congress targeted ‘Big Oil’ (specifically BP, Exxon Mobil, Shell, Chevron, and ConocoPhillips) in 1975 from being able to use this portion of the tax code.

The Tax Reduction Act of 1975 (TRA) changed two important components of the income tax law, which apply to petroleum producers. First, it repealed percentage depletion on a large proportion of crude oil and natural gas output [from Big Oil]. Second, it modified the calculation and use of the foreign tax credit by U.S. international oil companies. Title V of TRA repeals the 22-percent percentage depletion allowance on all oil and gas production for tax years ending after December 31, 1974, except for two exemptions.

First, domestic natural gas production meeting certain conditions will still qualify for percentage depletion under section 613 of the Internal Revenue Code. Second, domestic producers and royalty owners who can qualify as “independents” will be permitted percentage depletion deductions according to a schedule of maximum quantities and percentage rates which gradually phases down to a minimum floor for 1984 and later years.

So, Big Oil was targeted in the seventies, and Big Oil lost its right to use this tax provision.

Expensing of Exploration & Development Costs (26 U.S. Code 263(c) and 291)

This incentive is more commonly referred to as “Intangible Drilling Costs (IDCs).” The EIA has reported a maximum of $573 million in tax breaks using this portion of the code.

For other industries, this tax break is more commonly known as expensing of Cost of Goods Sold (COGS), and it has existed since the beginning of the income tax code. Unlike COGS, which can deduct 100% of its equipment in the first year (e.g. section 179 and others), the oil and gas industry has been severely limited and is only able to deduct 60-80% of each Tesla car equivalent (COGS).

Similar to our research on Percentage Depletion, Big Oil has been severely limited in its ability to use this portion of the tax code. Congress severely limited this incentive for ‘Big Oil’ in 1986 and again in 1992. Since 1986, corporations have only been able to deduct 70% of IDCs immediately, and the rest spread over 5 years.

Thus, the oil and gas industry does not then benefit from special treatment. In fact, any industry allowed to depreciate the entirety of COGS receives special tax treatment by comparison to the oil and gas industry.

Part II Conclusion

Contrary to what Google might indicate, oil and gas companies do not receive a single dollar in direct subsidies. Oil and gas companies also do not receive special tax treatment from the Internal Revenue Service. Despite our findings, oil and gas is still improperly attributed with $5.5 billion in Direct Subsidies and Tax Breaks according to the EIA nearly all of which is in the form of Tax Breaks (remember, tax breaks are not an actual subsidy according to the dictionary).

The overwhelming winner of the subsidies handouts out in the United States are the Wind, Solar, and Biofuels industries. Full stop.

As we continue our SUBSIDIES SERIES, we will examine the following together in the coming weeks:

The International Energy Agency’s expansion of the EIA’s definition to include consumer-facing subsidies (e.g. LIHEAP)

The International Monetary Fund’s expansion of the IEA’s definition of “post-tax subsidies”

New Metric: EIA Subsidies per usable energy (dollars per megawatt-hour)

Who Actually Pays Taxes

Summary Conclusions

Don’t want to miss out? Know someone who needs to hear the knowledge being dropped? Make sure they join this newsletter!